Contact us for

Contact us for 0

0

SHOPPING CART

SGD 0.00

133 New Bridge Road, Chinatown Point #10-03 Singapore 059413

133 New Bridge Road, Chinatown Point #10-03 Singapore 059413  +65 9061 2851 (Whatsapp) 24 Hrs

+65 9061 2851 (Whatsapp) 24 Hrs  contact@aceglobalaccountants.com

contact@aceglobalaccountants.com

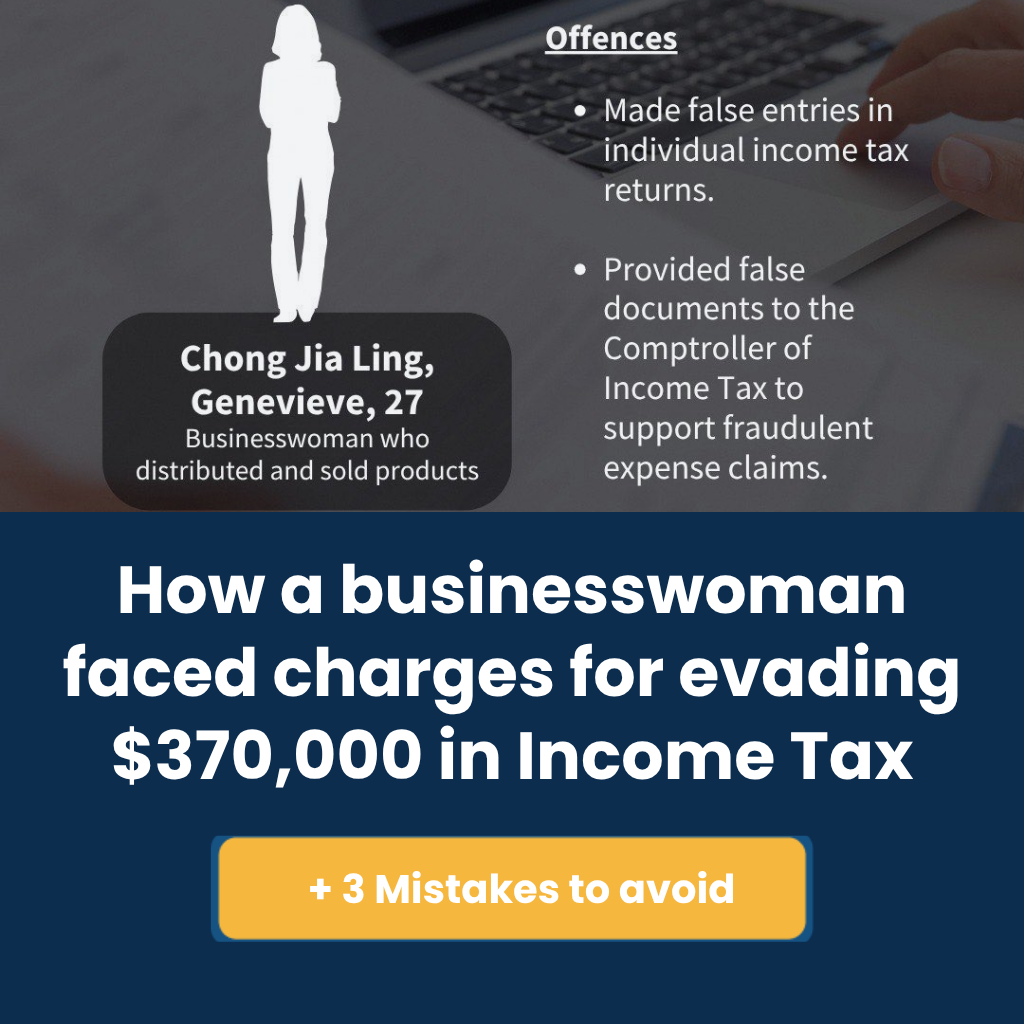

Two men — one 40, the other 73 — were about to be charged in court for their suspected role in a GST Missing Trader Fraud scheme worth $181 million.

Think about that number for a second, SGD 181 million. The alleged fraud wasn’t about sophisticated offshore structures or hidden assets. Instead, it came down to something deceptively simple: fictitious sales.

In this article, we’ll break it all down: the mechanics of such fraud, what this particular case signals for the business landscape in Singapore, and the steps you can take to stay compliant.

In early August 2025, Singapore’s Commercial Affairs Department (CAD) and the Inland Revenue Authority of Singapore (IRAS) announced charges against two men — aged 40 and 73 — for their suspected involvement in a Goods and Services Tax (GST) Missing Trader Fraud scheme worth approximately $181 million.

The case is one of the largest of its kind in recent years and serves as a strong reminder for businesses about the risks of fraudulent arrangements and the importance of due diligence.

At the centre of the alleged scheme were four shell companies set up between November 2017 and April 2018.

Here’s how investigators believe the fraud was carried out:

In total, the men allegedly tried to cheat IRAS into disbursing $11.8 million in fraudulent GST refunds.

In addition, the 40-year-old man is accused of going even further by:

If convicted, both men face heavy penalties:

These penalties underscore how seriously Singapore takes financial and tax-related offenses.

Fictitious sales are transactions that exist only on paper. They may involve:

The purpose of fictitious sales in this case was to create the illusion of business activity and claim GST refunds from the government. By showing “input tax” on these sham purchases, fraudsters attempted to cheat IRAS into paying money they were never entitled to.

For businesses, the danger is that even if you unknowingly participate in such a chain of transactions, you could still face penalties if you fail to spot the red flags.

To address this, Singapore has introduced stricter measures:

If you are GST-registered, here are some practical steps you should take:

For more information, please refer to the e-Tax Guide GST: Guide on Due Diligence Checks to Avoid Being Involved in Missing Trader Fraud.

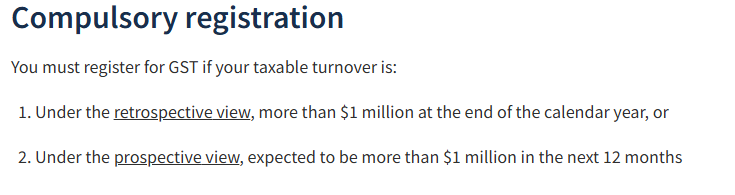

What is more, there is a hidden revenue threshold most Singapore companies are not even aware of when it comes to GST.

What many business owners don’t realise is that GST registration in Singapore becomes compulsory once your taxable turnover exceeds S$1 million in a 12-month period.

IRAS guideline on compusory GST registration

Unfortunately, many SMEs are simply not aware of this rule or don’t have proper systems to monitor their turnover closely.

If you are running a business in Singapore, you must:

When done right, these steps not only keep you compliant but also protect your reputation in the eyes of regulators, partners, and customers.

To learn more about GST in Singapore, you can read our article about Goods and Services Tax here.

We understand that for many busy business owners, keeping up with tax rules, GST thresholds, and compliance requirements can feel overwhelming.

If you’re unsure whether you’re at risk of crossing the S$1 million GST registration threshold or whether your current record-keeping is sufficient, that’s where we come in.

We can help you

If your company needs help filing taxes for the year 2025 or requires assistance with Singapore incorporation, economy, banking, etc., feel free to call /WhatsApp us at +65 90612851 or email us at aceglobalacct@gmail.com. Alternatively, you may leave us a reply using our contact form below.

Keep in touch to receive the latest listing, news updates and special offers delivered directly to your inbox.